Mortgage rates are still one of the biggest factors shaping the New York City real estate market in 2026.

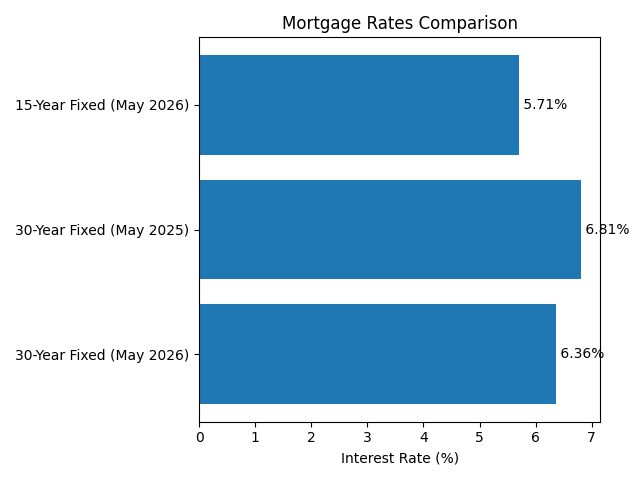

As of May 14, 2026, Freddie Mac reported the average 30-year fixed mortgage rate at 6.36%, down slightly from the prior week and lower than the 6.81% rate reported one year earlier. The 15-year fixed mortgage averaged 5.71%.

That is not a “cheap money” environment. But it is also no longer the shock that buyers felt when rates first moved up. The market has had time to adjust. Serious buyers are no longer asking only, “When will rates come down?” They are asking a smarter question: Does this apartment make sense at today’s price, today’s rate, and today’s monthly payment?

That is the right way to think.

NYC Buyers Cannot Only Watch the Rate

In New York, the mortgage rate is important, but it is not the whole story.

A buyer’s real monthly cost also includes maintenance or common charges, real estate taxes, insurance, possible assessments, and closing costs. In a co-op, the building may also require strong post-closing liquidity. That means a buyer needs to look beyond the headline rate and understand the full cost of ownership.

This is where many buyers make a mistake. They wait for the “perfect” rate, but they are not financially ready when the right apartment appears. In NYC, that can be costly. If rates move down meaningfully, more buyers may return to the market at the same time. Better inventory can become more competitive very quickly.

The strongest buyer is not always the one waiting the longest. It is often the one who has already spoken with a lender, understands the monthly payment, has documents ready, and can move with confidence.

What This Means for Sellers

Sellers also need to understand the impact of mortgage rates.

When rates are elevated, buyers become more selective. They compare more carefully. They calculate every monthly cost. They are less likely to stretch for an apartment that feels overpriced or financially unclear.

That does not mean sellers must give the property away. It means pricing needs to be intelligent. A beautiful apartment can still sit if the monthly carrying cost feels too high compared with similar options. On the other hand, a well-priced property with a clear value story can still attract serious attention.

In this market, buyers are not just buying the apartment. They are buying the monthly number.

The Bottom Line

Mortgage rates in mid-2026 are still elevated, but the market is no longer frozen.

For buyers, the best strategy is not to wait passively for a better rate. The best strategy is to understand your numbers, prepare your financing, and be ready when the right property appears.

In New York City, opportunity often arrives before the headlines feel comfortable.

0 Comments