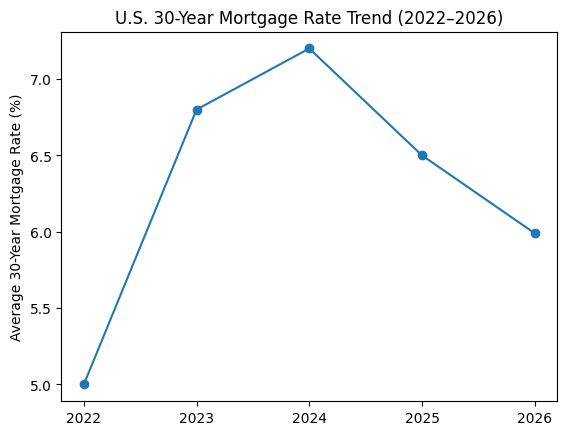

After several years of elevated borrowing costs, U.S. mortgage rates have finally dropped below 6%, offering welcome relief to homebuyers.

The average 30-year fixed mortgage rate recently fell to about 5.99%, marking the lowest level since 2022. The decline comes after rates hovered near 7% throughout much of the past two years, which significantly slowed homebuying activity.

For many buyers who were waiting on the sidelines, this drop could improve affordability and reignite housing demand in 2026.

Why Mortgage Rates Are Falling

Mortgage rates are influenced by broader financial markets, particularly U.S. Treasury yields and inflation expectations.

Several factors have contributed to the recent decline:

- Cooling inflation, easing pressure on borrowing costs

- Lower bond yields, which typically push mortgage rates down

- Shifting expectations around Federal Reserve policy

While rates fluctuate frequently, the move below 6% signals a meaningful improvement compared to recent years.

What Lower Rates Mean for Buyers

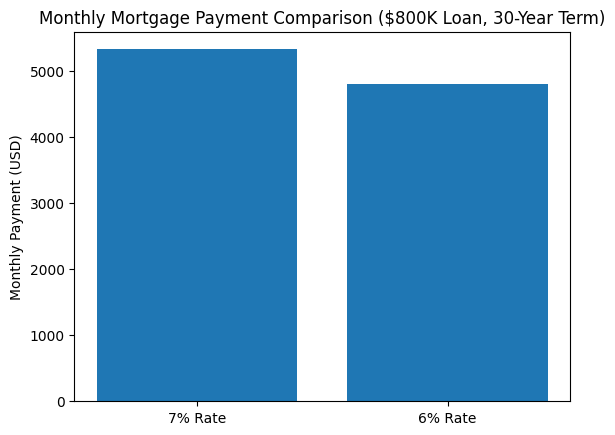

Even small changes in mortgage rates can significantly impact affordability.

Lower mortgage rates can:

- Increase purchasing power

- Reduce monthly payments

- Encourage more homebuying activity

For example, on a typical mortgage, a 1% drop in interest rates can increase buying power by roughly 10%.

Recent rate declines have already triggered an increase in mortgage applications and refinancing activity, suggesting buyers are starting to respond.

Outlook for the Housing Market

While mortgage rates remain higher than the ultra-low levels seen during the pandemic, the recent decline could help stabilize the housing market.

If rates stay near the 6% range throughout 2026, analysts expect:

- More buyer activity

- Increased refinancing opportunities

- Gradual improvement in housing affordability

For buyers who paused their search during higher rate periods, this shift could create new opportunities in the housing market.

Final Thoughts

The drop in mortgage rates below 6% marks an important turning point for the housing market.

While affordability challenges still exist, lower borrowing costs could help bring buyers back into the market and boost housing activity in 2026.

0 Comments